Author: Icon8888 | Publish date: Sat, 11 Jul 2015, 01:06 PM

Compared to other furniture stocks, Poh Huat's share price has not been so dynamic.

I believe this is due to perception that Poh Huat's business is seasonal.

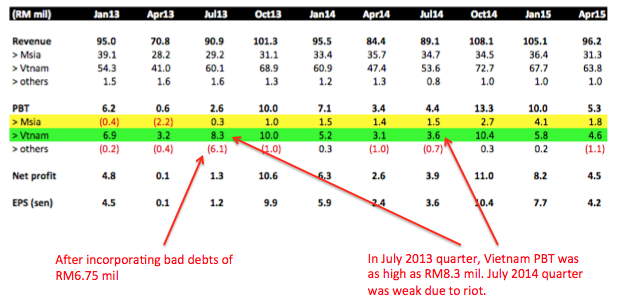

Referring to table below, many people would have concluded that October and January are strong quarters, while April and July are weak quarters.

If that is true, then the coming July quarter results, to be released by end September 2015, will continue to be weak. Excitement will only come in by end of December 2015 (6 months from now) when the October quarter is released.

As such, many people feel that the stock is unlikely to go anywhere from now until December 2015.

With that perception, no wonder Poh Huat share price has been lethargic.

However, as I took a closer look at Poh Huat's historical figures, I discover that this is not necessarily the case.

Contrary to popular belief, Poh Huat only has ONE weak quarter (the April quarter that was just released last week). The coming July quarter will be strong.

The reason is because the FY2013 July quarter was distorted by provision of bad debts of RM6.75 mil while the FY2014 July quarter was distorted by riot in Vietnam, which adversely affected Poh Huat's operation.

(Angry crowd is bad for business)

It was just a conincidence that in both years, certain bad things happened during July quarter !!!

Without those exceptional items, July quarter net profit for FY2013 and FY2014 would have been RM9.35 mil and RM9.8 mil, translating into EPS of 8.3 sen and 8.7 sen respectively.

Compared to FY2013 and FY2014, this coming July quarter result will be boosted by the following :-

(a) Weakening of Ringgit In FY2013 and FY2014, Ringgit / USD was 3.13 and 3.27. In July 2015 quarter, the exchange rate was easily 3.65.

(b) Turning Around of Malaysian operation In July quarter of FY2013 and FY2014, Malaysia operation generated PBT of RM0.3 mil and RM1.5 mil respectively. With revamping of its operation, Malaysia division nowadays generates PBT of RM2 to RM4 mil easily.

However, tax rate could be higher. In latest quarter ended April 2015, tax rate was 17% instead of zero.

Taking all these into consideration, it is not inconceivable that Poh Huat's coming July quarter EPS could be closed to 10 sen.

With share price at RM2.19, that kind of EPS should get many people excited and trigger a re-rating.

Bountiful harvest is near. Enjoy the fruits of your investment.

Thank you for sharing, Icon.

ReplyDelete