Steady Ship in Sea of Turbulence

Author: Icon8888 | Publish date: Fri, 12 Jun 2015, 01:54 PM

1. Introduction

I first wrote about Tong Herr in December 2014.

In this article, I will undertake a more indepth study of its operations and financial details.

Tong Herr Resources Berhad (THR) Snapshot

Open

2.05

|

Previous Close

2.13

| |

Day High

2.05

|

Day Low

2.02

| |

52 Week High

09/8/14 - 2.44

|

52 Week Low

10/16/14 - 1.88

| |

Market Cap

255.0M

|

Average Volume 10 Days

15.7K

| |

EPS TTM

0.23

|

Shares Outstanding

126.3M

| |

EX-Date

06/12/15

|

P/E TM

8.8x

| |

Dividend

0.12

|

Dividend Yield

5.94%

|

The group has been in operation for a long time, it is a very competent and experienced player. It did not do so well in 2012 and 2013 due to trade policy of certain countries. With the resolution of those issues, earnings had rebounced strongly in FY2014. Every quarter, they reported EPS of approximately 7 sen.

Annual Result:

| F.Y. | Revenue ('000) | Profit Attb. to SH ('000) | EPS (Cent) | PE | DPS (Cent) | DY | NAPS | ROE (%) |

|---|---|---|---|---|---|---|---|---|

| TTM | 587,698 | 29,068 | 22.99 | 8.79 | 12.00 | 5.94 | 2.8400 | 8.10 |

| 2014-12-31 | 562,439 | 30,138 | 23.84 | 8.48 | 11.00 | 5.45 | 2.7100 | 8.80 |

| 2013-12-31 | 519,999 | 17,596 | 13.91 | 12.51 | 4.00 | 2.30 | 2.5300 | 5.50 |

| 2012-12-31 | 484,398 | 14,654 | 11.56 | 15.32 | 22.00 | 12.43 | 2.4100 | 4.80 |

| 2011-12-31 | 601,065 | 36,554 | 28.73 | 6.83 | 8.00 | 4.08 | 2.5300 | 11.36 |

| 2010-12-31 | 344,279 | 25,387 | 19.93 | 13.05 | 5.00 | 1.92 | 2.3100 | 8.63 |

Quarter Result:

| F.Y. | Quarter | Revenue ('000) | Profit before Tax ('000) | Profit Attb. to SH ('000) | EPS (Cent) | DPS (Cent) | NAPS |

|---|---|---|---|---|---|---|---|

| 2015-12-31 | 2015-03-31 | 158,828 | 14,355 | 7,343 | 5.81 | 6.00 | 2.8400 |

| 2014-12-31 | 2014-12-31 | 149,945 | 3,868 | 3,280 | 2.59 | - | 2.7100 |

| 2014-12-31 | 2014-09-30 | 146,593 | 15,933 | 8,769 | 6.94 | 6.00 | 2.6300 |

| 2014-12-31 | 2014-06-30 | 132,332 | 16,279 | 9,676 | 7.65 | - | 2.6000 |

| 2014-12-31 | 2014-03-31 | 133,569 | 14,730 | 8,413 | 6.65 | 5.00 | 2.6000 |

The group has shareholders' funds of RM358 mil, cash of RM131 mil and borrowings of RM168 mil. This translates into net gearing of 0.10 times only.

Out of the borrowings of RM168 mil, approximately RM110 mil is in the form of Trust Receipts, which is a type of trade financing facility used to import raw materials. This type of facility is typically short term in nature, can be rolled over and bear low interest rate.

The group incurred interest expense of only RM2 mil+ per annum. Based on RM168 mil loans, effective interest rate is only 1.2%. This is a very important point as it shows that "high" borrowings does not really eat into profitability (another proof of the competence of management team).

2. Group Operation

The group is principally involved in manufacturing of fasteners (fancy name for nuts, bolts, screws, etc) and aluminium extrusion products.

(For those who wish to know more about aluminium extrusion, please refer to my old article about LB Aluminium)

http://klse.i3investor.com/blogs/icon8888/56467.jsp

The fastener division comprises a 100% owned subsidiary in Malaysia (Tong Herr Fasteners Co Sdn Bhd), a 51% owned subsidiary in Thailand (Tong Herr Fasteners (Thailand) Co Ltd).

The aluminium extrusion division is represented by 51% owned subsidiary Tong Herr Aluminium Industries Sdn Bhd.

Manufactruing plants are located at Perai (Penang) and Chonburi (Thailand).

The group also owns 32% effective equity interest in Vietname associate company Fuco Steel Corporation LTd, which manufacture steel billets.

(Province of Chonburi)

Based on estimates, the abovementioned entities reported the following earnings in FY2014 :-

| FY2014 PAT | Proportionate | |

| (RM mil) | (RM mil) | |

| Malaysia fasteners (100%) | 20.0 | 20.0 |

| Thailand fasteners (51%) | 14.0 | 7.1 |

| Malaysia aluminium extrusion (51%) | 9.9 | 5.1 |

| Vietname steel associate (32%) | (6.3) | (2.0) |

| TOTAL | 37.6 | 30.2 ^ |

^ FY2014 group net profit

For more details on how I derived the net profit of the various entities, please read on.

3. Historical Profitability

The following figures are derived from quarterly reports and annual reports. Please read the notes below the table for further details. For example, if you see "(a)" in the table, please scroll down the article to read the explanation (a).

| (RM mil) | Mar14 | Jun14 | Sept14 | Dec14 | FY2014 | Mar15 |

| Revenue (a) | 133.6 | 132.3 | 146.6 | 150.0 | 562.4 | 158.8 |

| > Fasteners | 94.9 | 91.6 | 106.2 | 113.5 | 406.3 | 119.3 |

| > Aluminium products | 38.7 | 40.7 | 40.4 | 36.4 | 156.2 | 39.5 |

| > others | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 |

| EBITDA | 19.8 | 18.8 | 21.1 | 15.1 | 74.9 | 23.8 |

| EBITDA margin (%) | 14.8 | 14.2 | 14.4 | 10.1 | 13.3 | 15.0 |

| Depreciation | (4.5) | (4.5) | (4.1) | (4.6) | (17.8) | (4.5) |

| Interest exp | (0.5) | (0.6) | (0.3) | (0.6) | (2.0) | (0.5) |

| interest income | 0.5 | 0.6 | 0.7 | 1.1 | 2.9 | 0.6 |

| Forex (b) | (0.2) | 1.4 | (1.8) | (4.7) | (5.2) | (2.6) |

| Derivatives (b) | (0.1) | (0.3) | 2.3 | 0.4 | 2.3 | 3.6 |

| Associate (c) | (0.4) | 0.6 | 0.3 | (2.4) | (2.0) | (2.4) |

| PBT | 14.7 | 16.3 | 15.9 | 3.9 | 50.8 | 14.4 |

| Tax | (3.0) | (3.0) | (3.1) | 0.1 | (9.0) | (3.3) |

| PAT | 11.7 | 13.3 | 12.9 | 4.0 | 41.8 | 11.1 |

| > Fasteners (Total) | 8.3 | 8.6 | 9.1 | 8.0 | 34.0 | 11.9 |

| > Fasteners (Malaysia) | 5.4 | 5.4 | 4.2 | 5.1 | 20.0 | |

| > Fasteners (Thailand) | 2.9 | 3.2 | 4.9 | 3.0 | 14.0 | |

| > Aluminium (Malaysia) | 3.8 | 4.1 | 3.5 | (1.6) (d) | 9.9 | 1.6 (d) |

| > others | (0.4) | 0.5 | 0.3 | (2.5) | (2.1) | (2.4) |

| MI | (3.3) | (3.6) | (4.1) | (0.7) | (11.70) | (3.8) |

| > Fasteners (Malaysia) | 0.0 | 0.0 | 0.0 | 0.0 | 0.00 | |

| > Fasteners (Thailand) | (1.4) | (1.6) | (2.4) | (1.4) | (6.72) | |

| > Aluminium (Malaysia) | (1.9) | (2.0) | (1.7) | 0.8 | (4.94) | |

| Net profit | 8.4 | 9.7 | 8.8 | 3.3 | 30.1 | 7.4 |

| > Fasteners (Malaysia) | 5.4 | 5.4 | 4.2 | 5.1 | 20.0 (e) | |

| > Fasteners (Thailand) | 1.5 | 1.6 | 2.5 | 1.5 | 7.1 | |

| > Aluminium (Malaysia) | 2.0 | 2.1 | 1.8 | (0.8) | 5.1 | |

| > others | (0.4) | 0.5 | 0.3 | (2.5) | (2.1) |

Some key observations :-

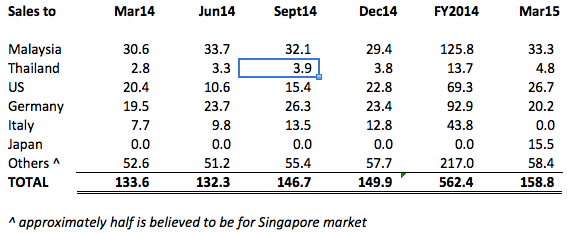

(a) Approximately 78% of the group's products are exported.

(b) The group is exposed to forex risk as it sells most of its products overseas and also has substantiual amount of forex loans. Probably caught offguard by the sharp depreciation of RM, it reported a forex loss of RM4.7 mil in December 2014 quarter, which dragged down group earnings substantially.

However, there is also a "Derivative" item which probably constitues forex hedging instruments. The drivative products flexed its muscle in March 2015 quarter by making a gain of RM3.6 mil, offseting the RM2.6 mil forex loss.

(c) The 32% owned associate company is Vietnam based and is principally involved in steel billet manufacturing. Its recent performance is disconcerting, with losses increases to approximately RM2.4 mil per quarter in December 2014 and March 2015 respectively.

Very little is known about this entity and its prospects. But I foresee it continues to bleed in coming quarters.

(d) The 51% owned subsidiary that manufactures aluminium extrusion products traditionally contributes approximately RM4 mil PAT per quarter (approximately RM2 mil Net Profit per quarter based on 51% equity interest).

However, in December 2014 quarter, this subsidiary reported a loss of RM1.6 mil. The company did not provide explanation and details. However, based on LB Aluminium's case, my guess is that its raw material cost has increased due to higher aluminium price and weakening of Ringgit.

The following is LB Aluminium's explanation in its January 2015 quarterly report for its decline in profitability :-

Fortunately, it seemed that performance for this division has stabilised as it reported PAT of RM1.6 mil in March 2015 quarter. The improvement could be partially due to decline of aluminium prices (please refer to chart below).

(e) The Malaysia subsidiary that manufactures fasteners is the biggest contributor to net profit by virtue of its huge profitability (RM20 mil net profit per annum) and fully owned status.

4. Concluding Remarks

(a) Overall performance has been dragged down by losses at associate level (steel billet manufacturing in Vietnam). The group needs to manage this proactively so as to limit further deterioration.

(b) Aluminium extrusion division was affected by higher raw material cost, but has turned around in latest quarter. Hopefully the recent softer aluminium price could help earnings to improve going forward.

(c) At current price, PER is approximately 9 times. But dividend yield is attractive at more than 5.5% (based on 12 sen DPS and share price of RM2.05). Even though not all things are rosy, I still like this group for its steady performance and trustworthy management team.

A HOLD for me.

No comments:

Post a Comment