Author: Icon8888 | Publish date: Sun, 12 Jul 2015, 11:47 AM

1. Introduction

Similar to Media Chinese International Ltd ("MCIL"), Media Prima saw dramatic decline in earnings since Mar 2014 due to softer market sentiment caused by air incidents, GST, soft oil price, political uncertainties, etc.

From an all time high of RM3.00, share price has declined by more than 57% to reach RM1.29.

Quarter Result:

| F.Y. | Quarter | Revenue ('000) | Profit Attb. to SH ('000) | EPS (Cent) | DPS (Cent) | NAPS |

|---|---|---|---|---|---|---|

| 2015-12-31 | 2015-03-31 | 329,389 | 18,883 | 1.70 | - | 1.4530 |

| 2014-12-31 | 2014-12-31 | 384,699 | -29,494 | -2.67 | 5.00 | 1.4359 |

| 2014-12-31 | 2014-09-30 | 379,598 | 42,176 | 3.82 | 3.00 | 1.4918 |

| 2014-12-31 | 2014-06-30 | 388,580 | 35,830 | 3.24 | 3.00 | 1.4834 |

| 2014-12-31 | 2014-03-31 | 351,030 | 27,016 | 2.45 | - | 1.5005 |

| 2013-12-31 | 2013-12-31 | 451,556 | 63,439 | 5.81 | 8.00 | - |

| 2013-12-31 | 2013-09-30 | 439,277 | 63,516 | 5.82 | 3.00 | 1.4767 |

| 2013-12-31 | 2013-06-30 | 466,274 | 60,103 | 5.52 | 3.00 | 1.4478 |

| 2013-12-31 | 2013-03-31 | 365,836 | 27,107 | 2.50 | - | 1.4595 |

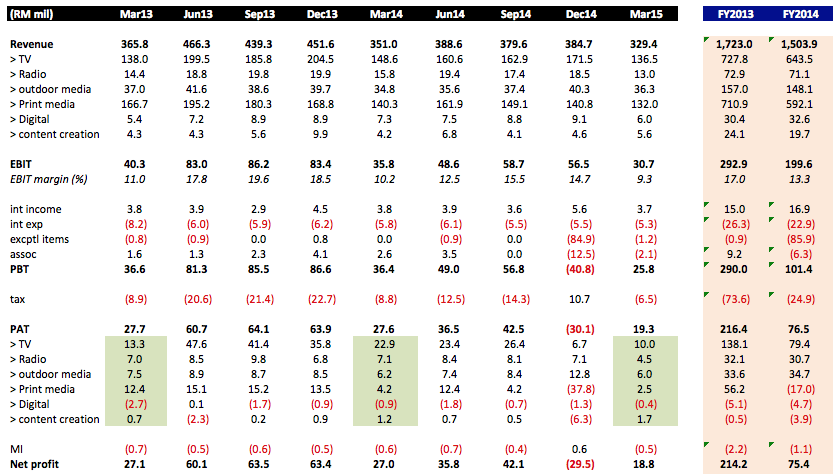

2. Past Few Quarters Performance

The table below sets out Media Prima's past two years' performance :-

Similar to MCIL, net profit experienced drastic drop in June 2014 quarter (50% drop y-o-y) affected by various factors as mentioned above. Since then, it has remained at a depressed level.

Revenue declined by 13% from RM1.72 billion in FY2013 to RM1.50 billion in FY2014. EBIT declined by 32% from RM293 mil to RM200 mil. EBIT margin experienced contraction from 17% to 13.3%.

Main culprits were the Free to Air TV ("FTA TV") and print media divisions.

In Q1 of FY2015, the group reported net profit of RM18.8 mil only. However, traditionally, this quarter is always the weakest in a year. Next quarter earnings should be stronger q-o-q.

3. Mutual Seperation Scheme ("MSS")

In December 2014, Media Prima undertook an MSS to trim its workforce. Altogether, 4,600 employees participated in the MSS which cost the group RM78.9 mil (RM17,000 per head). The group expects to recoup the amount within 2 years.

I believe the bulk of the MSS was at NSTP and Pay TV level (please refer to Q4 2014 PAT figures in the table above which saw drastic drop in earnings at these two divisions).

4. Concluding Remarks

2014 has been a bad year for media companies. 2015 will continue to be tough.

Due to the subdued sentiment, I am not really in a mood to undertake a comprehensive analysis at this stage. The objective of this article is just to lay out some details of the group's past few quarters' performance for everybody to have a feel.

Having said so, I am tracking Media Prima closely for entry opportunities. The group is an established player with solid track record. It pays out 11 sen dividend in 2014. Based on existing price, the yield is 8.5%. Even though it is unlikely to repeat the same payout this year, a 50% reduction to 5.5 sen will still yield 4.2%.

Media companies are sensitive to economic performance. When consumer sentiment improves, they will snap back with a vengeance.

If you are a long term investor, maybe you should pay some attention to this group going forward.

No comments:

Post a Comment