Author: Icon8888 | Publish date: Wed, 11 Nov 2015, 02:27 PM

1. Introduction

I first wrote about Jaycorp in March 2015 when it was trading at approximately 73 sen.

Since then, more than half a year had passed and three quarterly results had been released. Jaycorp is now trading at RM1.01. How has the company been performing ? Is it living up to its potential and shareholders' expectations ?

Quarter Result:

| F.Y. | Quarter | Revenue ('000) | Profit before Tax ('000) | Profit Attb. to SH ('000) | EPS (Cent) | DPS (Cent) |

|---|---|---|---|---|---|---|

| 2015-07-31 | 2015-07-31 | 69,295 | 3,031 | 1,821 | 1.33 | 4.00 |

| 2015-07-31 | 2015-04-30 | 59,606 | 6,522 | 3,992 | 2.92 | - |

| 2015-07-31 | 2015-01-31 | 54,733 | 1,320 | 1,023 | 0.75 | - |

| 2015-07-31 | 2014-10-31 | 64,274 | 3,462 | 1,156 | 0.85 | - |

| 2014-07-31 | 2014-07-31 | 59,946 | 3,383 | 1,706 | 1.25 | 3.50 |

| 2014-07-31 | 2014-04-30 | 54,751 | 2,984 | 2,172 | 1.59 | - |

| 2014-07-31 | 2014-01-31 | 63,878 | 3,615 | 2,481 | 1.85 | - |

| 2014-07-31 | 2013-10-31 | 57,752 | 3,612 | 2,210 | 1.62 | - |

As shown in table above, for the quarter ended 31 July 2015, the group reported net profit of RM1.82 mil only (EPS of 1.33 sen). By all measures, the results were disappointing. As a result, I have ignored this stock over past few months.

However, this morning I saw the stock flashing green in a sea of red, so I decided to take a closer look. What I discovered was astounding. Jaycorp's poor July 2015 quarterly results was mostly caused by exceptional items. Without those exceptional items, the group's net profit for July 2015 quarter would be as high as RM4.7 mil (EPS of 3.4 sen). If this figure is annualised, EPS could be as high as 13.6 sen. The current share price of RM1.01 translates into PER of 7.4 times.

(Please note : I have absoluetly no idea why the stock was so actively traded this morning and why it went up. I don't belong to any syndicate and I don't pump and dump. I am just a lonely old man trying to make a few quick bucks in the stock market)

2. Background Financials

Based on 137 mil shares and share price of RM1.01, market cap is RM138 mil.

The group has loans of RM26.7 mil, cash of RM23.1 mil and net assets of RM128.8 mil. As such, net gearing is only 0.03 times.

Based on FYE 31 July 2015 net profit of RM8 mil, historical PER is 17.3 times.

3. Past Few Quarters' Performance

Key observations :-

(a) Furniture division's revenue jumped to an all time high of RM57 mil in July 2015 quarter. Exact reasons unknown. It could be due to a combination of weak Ringgit (translation gain) and / or revenue contribution by newly acquired 51% owned Instyle Sofa Sdn Bhd ("ISSB"). Jaycorp completed the acquisition of 51% equity interest in ISSB on 30 April 2015 so the July quarter would have factored in its contribution. ISSB reported revenue of RM19.2 mil in 2013 so revenue per quarter would be approximately RM5 mil.

Please refer to Part 2 of my articles if you wish to know more about ISSB.

The furniture division's PBT had also increased tremendously, growing from the usual approximately RM3 mil per quarter to RM6 mil per quarter. This was very likely due to margin expansion following weakening of Ringgit.

(b) The packaging division's revenue and PBT remained more or less the same throughout the various quarters. A very steady business, mosly to cater for the group's packaging requirement for its furniture division.

(c) As usual, the rubber wood division's profitability was erratic, fluctuating between loss of RM0.8 mil and profit of RM2.1 mil. This divsion was 51% owned by Jaycorp. Please refer to Part 1 and 2 of my articles for further details.

(d) Over the past two quarters, the renewable energy division's performance has stabilised. Loss before tax had been reduced from approximately RM1 mil to RM0.2 mil per quarter. According to the company, it was due to improvement in operational efficiency. Hopefully this division will start making positive contribution to PBT soon.

(e) The group reported a disappointing set of results for its July 2015 quarter with net profit of RM1.82 mil. However, the poor result was due to exceptional items amounting to RM4.6 mil (please refer to green highlighted section in table above). Excluding those items and factoring in effective tax rate, adjusted net profit will be approximately RM4.7 mil. Based on 137 mil shares, EPS for latest quarter was actually 3.4 sen.

4. Concluding Remarks

I was disappointed with Jaycorp when it released its July 2015 quarterly result in September 2015. If the group still cannot perform when Ringgit was trading at RM4+, will it ever perform ?

However, upon closer study, it seemed that the latest quarter result was distorted by exceptional items, which are non recurrent in nature.

As a matter of fact, the group's furniture division has already been behaving like a Pohuat, Lii Hen, Latitude Tree, etc... with PBT margin expanded from 6% to 11% as the Ringgit weakened.

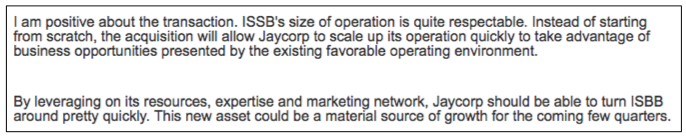

Going forward, ISSB will also start contributing to revenue and profitability. I am very positive about the acquisition when I wrote my earlier article (reproduced below) :-

In addition, the renewable energy division, which has been a drag in the past, is showing signs of turning around.

With Ringgit expected to remain weak over an extended period of time and all divisions doing well, the group's prospects looked promising.

Now you know why I called it a hidden gem.

No comments:

Post a Comment