1. Introduction

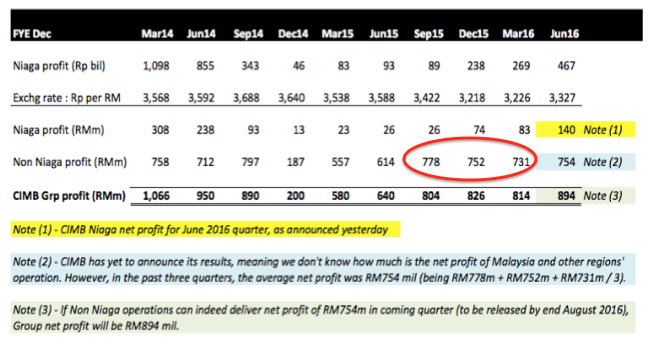

After I published Part 2 on 30 July 2016, a sharp eye reader made an interesting observation. He pointed out that the profitability of CIMB Non Niaga (namely Malaysia, Thailand and Singapore operations) has been on downward trend (down from RM778 mil to RM752 mil to RM731 mil).

(Note : the above table is extracted from Part 2)

Is Non Niaga's decline in profitability structural in nature ? This is an important question.

CIMB Niaga's recently released June 2016 quarterly result showed improvement. However, if Non Niaga's profit is indeed on "downward trajectory", the coming quarter overall result (to be released by end August 2016) might not be good.

To find out the answer, I decided to perform a more detailed analysis of the CIMB Group's past few quarters' performance.

2. Non Inerest Income Is The Main Culprit

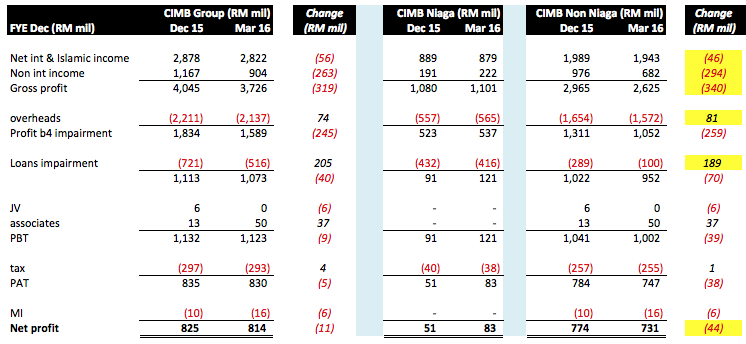

When I started my analysis, I intended to study three quarters : September 2015, December 2015 and March 2016. However, after taking a closer look, I noticed that the September 2015 quarter included expenses incurred for the Mutual Separation Scheme. The figures were quite messy and it is difficult to figure out how the entire CIMB Group has actually performed in that quarter. As such, I narrowed down my study to only the December 2015 and March 2016 quarter.

Key observations :-

(a) As mentioned above, Non Niaga's profit declined from RM774 mil in December 2015 to RM731 mil in March 2016, a decline of RM44 mil. What caused the decline ?

(b) Net interest income and Islamic banking income, which form the backbone of banking operations, was quite stable. There was a small decline of RM46 mil. In my opinion, that was not really that material.

(c) The biggest drop was actually caused by Non Interest Income, which declined by a whopping RM294 mil.

(d) As a result of the above, Gross profit declined by RM340 mil.

(e) Fortunately, Non Niaga's other operational parameters mostly improved. Overheads were reduced by RM81 mil while Loan Impairment was RM189 mil lower than previous quarter, collectively resulted in saving of RM270 mil.

(f) That helped to offset the bulk of the weakness seen in Non Interest Income.

Now that we have established that Non Interest Income is the main culprit, the next step is to find out what constitute Non Interest Income and whether it will continue to be weak in coming quarter.

3. Non Interest Income

Key observations :-

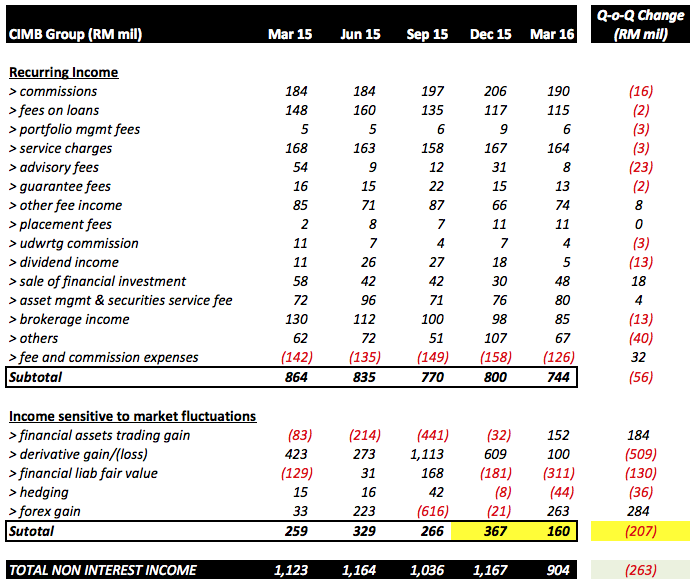

(a) CIMB provides detailed breakdown of its Non Interest Income. Pursuant to my analysis, they can be grouped under two major categories : (i) Recurring Income and (ii) Income sensitive to market fluctuations.

(b) Recurring Income includes those items such as commissions, advisory fees, brokerage income, etc. Please go through the list in the table above, which is self explanatory.

(c) Income Sensitive To Market Fluctuations comprise 5 major items :-

(i) financial assets trading gain;

(ii) derivative trading gain;

(iii) fair valuation of financial liabilities;

(iv) hedging; and

(v) forex gain.

(d) Unlike Recurring Income, these items are volatile in nature. For example, forex trading incurred a loss of RM616 mil in September 2015 and chalked up RM263 mil gain in March 2016.

(e) But please don't get me wrong. I am not saying that CIMB (or any other bank) engages in risky speculation. Banks are regulated by BNM. I am pretty sure that whatever they do, they must have done it with proper risk management measures in place.

You can actually see this through the combined figures. Despite huge swing of individual components, collectively these items generated profit within a narrow band of RM259 mil to RM367 mil.

(f) However, it seemed that luck was not on their side in the March 2016 quarter. Profit deviated substantially from the narrow band. That was mostly caused by larger than normal fair value loss for financial liabilties (RM311 mil, I have no idea what that is) and lower derivative gain (RM100 mil only, as compared to RM609 mil in previous quarter).

The end result was that Non Interest Income declined by RM263 mil.

4. Concluding Remarks

According to my analysis, the Q-o-Q decline in Non Niaga's profitability (comprises Malaysia, Thailand and Singapore operations) was not structural in nature. It was mostly caused by unfavorable luck factor in March 2016 quarter.

CIMB Niaga has already delivered a positive set of results recently. We are holding our breath, waiting to find out whether the other divisions can also perform well and deliver a strong set of results for the entire group.

Best of luck to all CIMB shareholders.

No comments:

Post a Comment