Publish date: Fri, 8 Jan 2016, 08:01 PM

(Note : To understand this article, you should first read Part 1, 2 and 3)

1. Introduction

In Part 1, I wrote about the difference between Value Traders and Value Investors.

In Part 2 and Part 3, I wrote about Value Traders such as Ooi Teik Bee and Uncle Koon. In Part 4, it is natural for me to zoom in on Value Investors.

But what should I study and talk about ? Unlike Value Trading, a term recently created by me, Value Investing has been in existence for more than 100 years. Faced with an ocean of information and knowledge, I am totally lost.

The inspiration came yesterday.

2. The Journey Of Discovery Began...

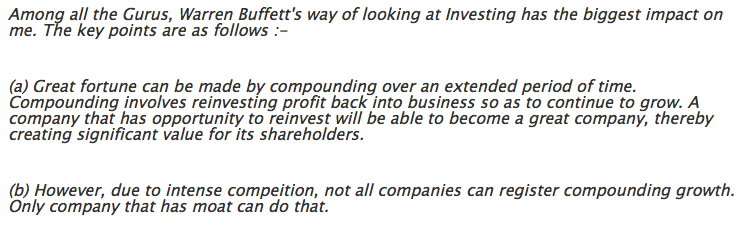

First of all, I am not operating out of a vacuum. When come to Value Investing, the following are what I have in mind (extracted from Part 1) :

After giving some thoughts, I arrived at the conclusion that the most meaningful topic is to try to figure out how Warren Buffett picked his stocks.

Hopefully that will lead me to insights on how to identify stocks that can compound growth Buffett style, something that my readers will be extremely interested in.

In order to do that, I first need to identify Malaysia stocks that Buffett would like to own.

I first tried out with Return On Invested Capital (ROIC) method. ROIC is widely used by the investment fraternity to identify companies with moat. The higher the ROIC, the stronger the moat.

My study turned out a few companies with high ROIC. For example, BAT has ROIC of more than 150% (anything higher than let's say 13% is considered ok). However, the finding did not excite me much. BAT seemed to have moat, but it doesn't look like a Buffett stock. I cannot explain in words, I simply cannot smell the money.

3. Sea Cucumber Breakthrough

Confused and frustrated, I decided to have my dinner first to refresh my mind.

While chewing on my beloved sea cucumber, suddenly I have a Eureka moment - Buffett Stocks should look like sea cucumber !!!

Sea cucumber have rings. Buffett stocks' operating profit must be able to grow year after year like the sea cucumber's series of rings !!!

Grow by how much ? 23% per annum !!! That is the magic figure for Buffett. By growing 23% a year for 20, 30 years, Buffett became the richest person in the world !!!

(You can set a lower target, but the whole idea is that the stock must have potential to grow consistently at that rate over a long preiod of time, if you want to play the Value Investing game)

THIS, is the definiing charatecristic of a Buffett stock. All other things are secondary.

Then I realised why I didn't find BAT attractive. This is how its historical profit looked like :-

As shown in table above, BAT reported net profit of RM782 mil in 2004. Ten years later in 2014, its profit grew by 15% to RM898 mil. Even if you add in the dividend, I can bet a bag of gold for your potato that the compounded return will be significantly less than 23% per annum.

If Warren Buffett has invested in BAT in 2004, his shareholders will be throwing shoes at him in AGM.

This small discovery is not something to be sneezed at. Its practical usefulness immediately shows up and shines.

For example, last time I thought Apollo is a Buffett stock (weak form). It has a brand, sells its products overseas (unlimited growth potential), excellent management, etc. But once I apply the Sea Cucumber Principle on it, it immediately disqualifies.

By using the Sea Cucumber Principle, I managed to pick up a few stocks that Buffett might like. One of them is Top Glove.

As shown in table above, within a period of 15 years, Top Glove grew its profit by 17.6 times, from RM15.9 mil to RM280 mil. Compounded growth rate works out to be approximately 21%. After adding in dividend of approximately 2% per annum, the compounded return will be exactly 23% !!!

Ladies and gentlemen, this is a Buffett stock. No financial analysis required, I can confrim that with you on the spot !!!

(The other few stocks are Hong Leong Financial Group, Dutch Lady, Public Bank. I will try to identify more when I am not busy cooking sea cucumber)

4. Buffett Came To The Rescue

Well, so far I managed to score one small victory. I have nailed down how a Buffett stock should look like (as far as I am concerned).

The next task is to try to figure out how somebody can detect Top Glove way back in 2001. If there is indeed a formula, we would like to replicate it to make ourselves filthy rich !!!

Again, I pulled out my ROIC calculator and ran some figures. In Top Glove's early years, its ROIC was approximately 20%+. Pretty impressive. But according to my previous studies, there were quite a few other stocks that have these kind of ROIC (and none became Buffett stocks).

Once again, I am stuck. Cannot smell the money. Even sea cucumber also cannot help me this round.

I finally decided to flip through some Buffett related books for clues. One of the book, "The Warren Buffett Way", sheds some light on how Buffett picked his stocks.

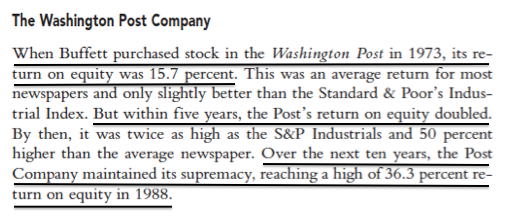

When Buffet buys a stock, the company does not necessarily have strong financial performance. For example, when Buffett bought into Washington Post in 1973, the company was not really doing so well.

As shown above, Washington Post's ROE at the time of Buffett's entry was more or less the same as its industry peers. Only five years later its performance made a quantum leap, exhibiting the kind of quality that Buffett Stocks typically possess.

But how did Buffett detect a good stock ?

The Book described the process quite well. Before Buffett bought into Washington Post, he was already quite familiar with the company. Buffett first met Washington Post's owner, Katherine Graham in 1971 and they have indepth discussions about the company (he bought into Washington Post in 1973).

What conclusion can we draw from the above ? The conclusion is that we shouldn't rely excessively on financial analysis to detect moat. Some of the moat that we detect by using financial analysis is "Existing Moat" (such as BAT). Existing Moat is useless for achieving capital gain, it will only lead us to buy into pricey blue chips.

What makes Buffett rich is "Potential Moat". To detect Potential Moat, we need to combine financial analysis with field research.

5. Concluding Remarks

(a) There is a sea of information out there regarding Value Investing. I used to feel very confused about how to do it. At one point, I tried to identify moat by relying on ROIC and other financial ratios.

(b) This latest study leads me to the conclusion that we should not purely rely on financial analysis to detect moat. We should try to combine it with field research and other sources of information (includes speaking to people in the industries).

(c) Alternatively, we should adopt a two track approach to investing. Since it is so difficult to detect potential moat, we should buy into stocks that suit our valuation yardstick even though they are not exhibiting moat. However, we should keep an eye out for keepers. If a particular stock is showing signs of sustainable growth, we should keep it for long term. Warren Buffett becomes the richest person in the world by letting his stocks compound. It would be nice if we can do that.

1. Introduction

In Part 1, I wrote about the difference between Value Traders and Value Investors.

In Part 2 and Part 3, I wrote about Value Traders such as Ooi Teik Bee and Uncle Koon. In Part 4, it is natural for me to zoom in on Value Investors.

But what should I study and talk about ? Unlike Value Trading, a term recently created by me, Value Investing has been in existence for more than 100 years. Faced with an ocean of information and knowledge, I am totally lost.

The inspiration came yesterday.

2. The Journey Of Discovery Began...

First of all, I am not operating out of a vacuum. When come to Value Investing, the following are what I have in mind (extracted from Part 1) :

After giving some thoughts, I arrived at the conclusion that the most meaningful topic is to try to figure out how Warren Buffett picked his stocks.

Hopefully that will lead me to insights on how to identify stocks that can compound growth Buffett style, something that my readers will be extremely interested in.

In order to do that, I first need to identify Malaysia stocks that Buffett would like to own.

I first tried out with Return On Invested Capital (ROIC) method. ROIC is widely used by the investment fraternity to identify companies with moat. The higher the ROIC, the stronger the moat.

My study turned out a few companies with high ROIC. For example, BAT has ROIC of more than 150% (anything higher than let's say 13% is considered ok). However, the finding did not excite me much. BAT seemed to have moat, but it doesn't look like a Buffett stock. I cannot explain in words, I simply cannot smell the money.

3. Sea Cucumber Breakthrough

Confused and frustrated, I decided to have my dinner first to refresh my mind.

While chewing on my beloved sea cucumber, suddenly I have a Eureka moment - Buffett Stocks should look like sea cucumber !!!

Sea cucumber have rings. Buffett stocks' operating profit must be able to grow year after year like the sea cucumber's series of rings !!!

Grow by how much ? 23% per annum !!! That is the magic figure for Buffett. By growing 23% a year for 20, 30 years, Buffett became the richest person in the world !!!

(You can set a lower target, but the whole idea is that the stock must have potential to grow consistently at that rate over a long preiod of time, if you want to play the Value Investing game)

THIS, is the definiing charatecristic of a Buffett stock. All other things are secondary.

Then I realised why I didn't find BAT attractive. This is how its historical profit looked like :-

| F.Y. | Revenue ('000) | Profit Attb. to SH ('000) | EPS (Cent) | DPS (Cent) | DY |

|---|---|---|---|---|---|

| 2014-12-31 | 4,795,991 | 898,125 | 315.90 | 78.00 | 1.20 |

| 2013-12-31 | 4,517,222 | 825,772 | 288.40 | 78.00 | 1.22 |

| 2012-12-31 | 4,364,786 | 798,394 | 279.40 | 272.00 | 4.39 |

| 2011-12-31 | 4,127,245 | 719,615 | 252.00 | 276.00 | 5.53 |

| 2010-12-31 | 3,965,448 | 731,111 | 256.10 | 240.00 | 5.33 |

| 2009-12-31 | 3,923,421 | 746,784 | 261.50 | 236.00 | 5.51 |

| 2008-12-31 | 4,135,220 | 811,683 | 284.30 | 265.00 | 5.96 |

| 2007-12-31 | 3,830,869 | 731,931 | 256.30 | 256.50 | 6.22 |

| 2006-12-31 | 3,612,482 | 719,678 | 252.00 | 254.00 | 5.87 |

| 2005-12-31 | 3,564,215 | 592,802 | 207.60 | 250.10 | 6.21 |

| 2004-12-31 | 3,263,725 | 782,084 | 273.90 | 248.40 | 5.43 |

As shown in table above, BAT reported net profit of RM782 mil in 2004. Ten years later in 2014, its profit grew by 15% to RM898 mil. Even if you add in the dividend, I can bet a bag of gold for your potato that the compounded return will be significantly less than 23% per annum.

If Warren Buffett has invested in BAT in 2004, his shareholders will be throwing shoes at him in AGM.

This small discovery is not something to be sneezed at. Its practical usefulness immediately shows up and shines.

For example, last time I thought Apollo is a Buffett stock (weak form). It has a brand, sells its products overseas (unlimited growth potential), excellent management, etc. But once I apply the Sea Cucumber Principle on it, it immediately disqualifies.

| F.Y. | Revenue ('000) | Profit Attb. to SH ('000) | EPS (Cent) | DPS (Cent) | DY |

|---|---|---|---|---|---|

| 2015-04-30 | 212,627 | 25,294 | 31.62 | 25.00 | 5.53 |

| 2014-04-30 | 220,506 | 33,470 | 41.84 | 25.00 | 5.22 |

| 2013-04-30 | 222,746 | 32,084 | 40.11 | 20.00 | 5.25 |

| 2012-04-30 | 200,548 | 21,744 | 27.18 | 20.00 | 6.83 |

| 2011-04-30 | 176,292 | 17,854 | 22.32 | 25.00 | 8.20 |

| 2010-04-30 | 159,531 | 24,677 | 30.85 | 20.00 | 6.90 |

| 2009-04-30 | 175,337 | 20,918 | 26.15 | - | - |

| 2008-04-30 | 181,144 | 20,975 | 26.22 | - | - |

| 2007-04-30 | 154,272 | 24,554 | 30.69 | 25.00 | 8.99 |

| 2006-04-30 | 142,370 | 20,762 | 25.95 | 20.00 | 7.75 |

By using the Sea Cucumber Principle, I managed to pick up a few stocks that Buffett might like. One of them is Top Glove.

| F.Y. | Revenue ('000) | Profit Attb. to SH ('000) | EPS (Cent) | PE | DPS (Cent) | DY | ROE (%) |

|---|---|---|---|---|---|---|---|

| 2015-08-31 | 2,510,510 | 280,145 | 45.36 | 17.02 | 20.00 | 2.59 | 17.58 |

| 2014-08-31 | 2,275,366 | 180,523 | 29.09 | 16.47 | 16.00 | 3.34 | 12.93 |

| 2013-08-31 | 2,313,234 | 196,500 | 31.72 | 19.36 | 16.00 | 2.61 | 14.48 |

| 2012-08-31 | 2,314,454 | 202,726 | 32.77 | 16.15 | 16.00 | 3.02 | 15.83 |

| 2011-08-31 | 2,053,916 | 113,091 | 18.29 | 26.58 | 11.00 | 2.26 | 9.89 |

| 2010-08-31 | 2,079,432 | 245,231 | 39.83 | 15.24 | 16.00 | 2.64 | 22.01 |

| 2009-08-31 | 1,529,077 | 169,133 | 28.01 | 24.82 | 11.00 | 1.58 | 20.30 |

| 2008-08-31 | 1,374,196 | 110,064 | 37.18 | 10.92 | 11.00 | 2.71 | 16.29 |

| 2007-08-31 | 1,228,778 | 89,560 | 31.20 | 22.60 | 9.22 | 1.31 | 14.63 |

| 2006-08-31 | 992,611 | 78,392 | 29.70 | 29.13 | 8.33 | 0.96 | 28.15 |

| 2005-08-31 | 641,827 | 58,141 | 31.04 | 16.11 | 8.00 | 1.60 | 27.86 |

| 2004-08-31 | 418,133 | 39,534 | 21.30 | 17.00 | 7.00 | 1.93 | 25.39 |

| 2003-08-31 | 265,089 | 25,258 | 27.71 | 7.15 | 12.00 | 6.06 | 19.57 |

| 2002-08-31 | 180,202 | 18,059 | 19.85 | 5.60 | 6.00 | 5.41 | 11.82 |

| 2001-08-31 | 138,862 | 15,901 | 28.85 | 3.12 | - | - | 15.48 |

As shown in table above, within a period of 15 years, Top Glove grew its profit by 17.6 times, from RM15.9 mil to RM280 mil. Compounded growth rate works out to be approximately 21%. After adding in dividend of approximately 2% per annum, the compounded return will be exactly 23% !!!

Ladies and gentlemen, this is a Buffett stock. No financial analysis required, I can confrim that with you on the spot !!!

(The other few stocks are Hong Leong Financial Group, Dutch Lady, Public Bank. I will try to identify more when I am not busy cooking sea cucumber)

4. Buffett Came To The Rescue

Well, so far I managed to score one small victory. I have nailed down how a Buffett stock should look like (as far as I am concerned).

The next task is to try to figure out how somebody can detect Top Glove way back in 2001. If there is indeed a formula, we would like to replicate it to make ourselves filthy rich !!!

Again, I pulled out my ROIC calculator and ran some figures. In Top Glove's early years, its ROIC was approximately 20%+. Pretty impressive. But according to my previous studies, there were quite a few other stocks that have these kind of ROIC (and none became Buffett stocks).

Once again, I am stuck. Cannot smell the money. Even sea cucumber also cannot help me this round.

I finally decided to flip through some Buffett related books for clues. One of the book, "The Warren Buffett Way", sheds some light on how Buffett picked his stocks.

When Buffet buys a stock, the company does not necessarily have strong financial performance. For example, when Buffett bought into Washington Post in 1973, the company was not really doing so well.

As shown above, Washington Post's ROE at the time of Buffett's entry was more or less the same as its industry peers. Only five years later its performance made a quantum leap, exhibiting the kind of quality that Buffett Stocks typically possess.

But how did Buffett detect a good stock ?

The Book described the process quite well. Before Buffett bought into Washington Post, he was already quite familiar with the company. Buffett first met Washington Post's owner, Katherine Graham in 1971 and they have indepth discussions about the company (he bought into Washington Post in 1973).

What conclusion can we draw from the above ? The conclusion is that we shouldn't rely excessively on financial analysis to detect moat. Some of the moat that we detect by using financial analysis is "Existing Moat" (such as BAT). Existing Moat is useless for achieving capital gain, it will only lead us to buy into pricey blue chips.

What makes Buffett rich is "Potential Moat". To detect Potential Moat, we need to combine financial analysis with field research.

5. Concluding Remarks

(a) There is a sea of information out there regarding Value Investing. I used to feel very confused about how to do it. At one point, I tried to identify moat by relying on ROIC and other financial ratios.

(b) This latest study leads me to the conclusion that we should not purely rely on financial analysis to detect moat. We should try to combine it with field research and other sources of information (includes speaking to people in the industries).

(c) Alternatively, we should adopt a two track approach to investing. Since it is so difficult to detect potential moat, we should buy into stocks that suit our valuation yardstick even though they are not exhibiting moat. However, we should keep an eye out for keepers. If a particular stock is showing signs of sustainable growth, we should keep it for long term. Warren Buffett becomes the richest person in the world by letting his stocks compound. It would be nice if we can do that.

No comments:

Post a Comment