Author: Icon8888 | Publish date: Tue, 15 Mar 2016, 12:04 PM

(Buffett was averse to airline stocks due to their low profit margin and heavy capex requirement. Will he change his mind now that oil is so cheap ?)

Executive Summary

(a) In the past few years, Air Asia has grown its fleet and revenue substantially, yet its profitability remained more or less the same. To find out why, I undertook a detailed study of the group's historical P&L.

(b) Pursuant to my analysis, high fuel cost (and the inability to pass through to passengers) is the main culprit.

(c) Current low oil price will unshackle the group, allowing it to keep price low and at the same time rake in healthy profit margin.

(d) As a conclusion, Air Asia is entering a golden era, with strong profit and potentially high dividend going forward. Maintained "Screaming Buy".

1. Introduction

Last week, after I published Part 1, many readers gave their comments. One in particular caught my attention - "Warren Buffett doesn't like airline stocks".

Without the need to cross check, I immediately know that the comment is very likely true.

This is because everybody knows that Warren Buffett likes strong free cashflow. You don't need to be an aviation expert to know that airline business is characterised by low margin and high capex. Some people describe it as "growing themselves into bankruptcy". This is the exact opposite of what Warren Buffett desires.

Is this stereotype applicable to Air Asia ? How has it performed in the past ? What actually dragged down its performance ? Are these inhibitors stil there ? Will they continue to affect the group going forward ?

2. Unpleasant Big Picture Indeed

The only way to answer those questions is to study the group's past performance.

First of all, we need to establish whether Air Asia meets Buffett's stereotype for airline companies.

Indeed, the group displayed certain characteristics of Buffett stereotype for airline companies :-

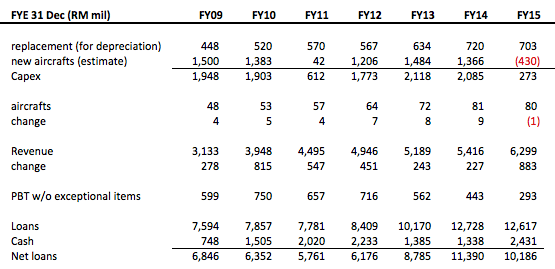

(a) Between FY2009 and FY2015 (a period of 7 years), Air Asia spent a total of RM10.7 billion on capital expenditure.

(b) The group increased its fleet size by 67% from 48 aircrafts to 80 aircrafts.

(c) In line with the fleet expansion, revenue also increased by 73% from RM3.13 billion to RM5.42 billion (I used FY2014 figure as 2015 was inflated by huge aircraft operating lease, as pointed out in my first article).

(d) Unfortunately, PBT (exlcudes exceptional items) remained stagnant throughtout the years.

(e) Net borrowings increased from RM6.85 billion to RM10.2 billion.

What had transpired ? What are the things that held back the group ?

To answer the above question, we need to take a closer look at the group's historical P&L.

The table above contains a lot of information. Unfortunately, it is a format that is not conducive for spotting patterns and trends.

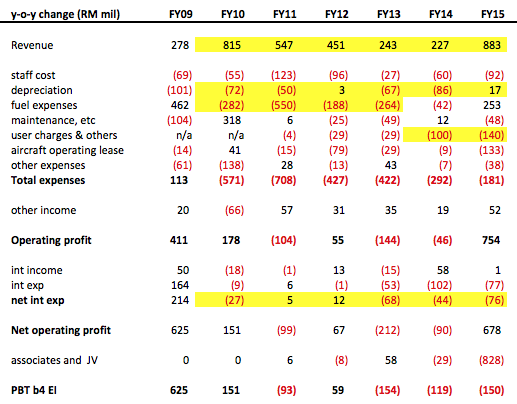

It turns out that by looking at year-on-year changes, the various major factors affecting Air Asia's profitability will immediately show up.

Just in case the readers do not understand how to read the above table, let me use revenue to demonstrate. For example, the FY2010 figure of RM815 mil = FY2010 revenue - FY2009 revenue = RM3,948 mil - RM3,133 mil.

Key observations :-

(a) Between FY2009 and 2015, average revenue growth was RM492 mil per annum.

(b) Despite heavy capex, depreciation charges had not grown by much. On average, the increase was around RM70 mil per annum. Not a small number, but relatively insignificant compared to average revenue growth of RM492 mil per annum. It is not the major culprit we are looking for.

(c) The same is true for interest expenses. The group's borrowings increased by 66% from RM7.6 billion in FY2009 to RM12.6 billion in FY2015. However, net interest expenses on average increased by RM33 mil per annum only. Again, it was relatively insignificant compared to annual revenue growth of RM492 mil per annum.

(Note : Further analysis showed that the relatively small increase in interest expenses was largely due to the group's ability to lower its cost of financing from 4.9% to 4.2% over the years)

(d) The item that has the biggest negative impact on group profitability turned out to be fuel expenses. As shown in table above, during the period from FY2010 until FY2013, average increase in fuel expenses was RM321 mil per annum. This item alone knocked off 65% of the increase in revenue from capacity expansion, leaving behind only 35% to cater for increase in other expenses. After deducting all the additional expenses, there is nothing much left for shareholders.

4. The Economics Of Fuel Surcharge

In my opinion, the high fuel cost experienced by Air Asia was actually a result of competitive pressure.

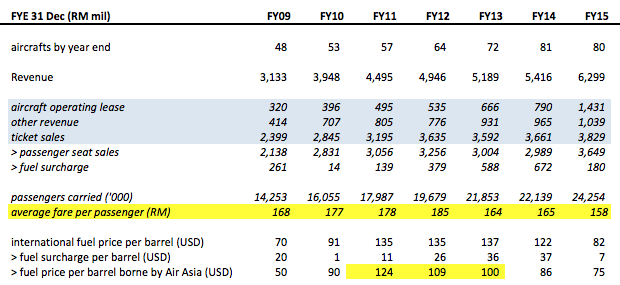

The group is entitled to pass on higher fuel cost to passengers. However, due to intense competition from MAS and other low cost operators, the group absorbed the bulk of the cost increase to defend market share. During the period under review, average fare per passenger was on downward trend despite persistently high oil price.

The effects of high fuel price was particularly pronounced during the period from 2011 to 2013. Even after passing on some of the cost to passengers by way of fuel surchage, average cost per barrel was still as high as USD111 per barrel.

That was the main reason why Air Asia was not able to grow its profit despite healthy top line growth.

However, there are signs that things are improving. In the latest quarter ended 31 December 2015, average fare has increased to RM178 per passenger.

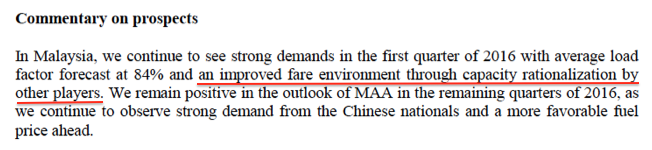

The improvement was likely due to MAS' rationalisation exercise which involved shutting down certain flight routes. The company made the following commentary in the December 2015 quarterly report :-

5. Cashflow

There are allegations that airline companies need to call on shareholders to inject capital every now and then. Is that the case for Air Asia ? Let's look at the group's historical cash flow to help us answer the question.

Key observations :-

(a) Good time or bad time, the group generated robust EBITDA of approximately RM1.5 billion per annum. I give that a big LIKE.

(b) The group spent heavily on capex (RM10.7 billion over a period of 7 years) to grow market share.

I reject the notion that the group is growing itself into bankruptcy.

As per my analysis above, profit stagnation was mostly due to high fuel cost and competitive pressure tying their hands. Now that we are entering an era of low oil price, many of the routes that previously struggled to break even should turn profitable.

On hind sight, the group has done the right thing by pushing ahead with capacity expansion in the face of high fuel cost. Without that, it won't be able to enjoy the current windfall gain brought by low oil price.

Opportunity is indeed for the prepared mind.

(c) During the period from FY2011 to 2015, the group injected RM743 mil capital into its associate companies and jointly controlled entities (Thai Air asia, Indonesia Air Asia, Philippine Air Asia, etc) by way of equity injection as well as shareholders' advances.

Apart from Thai Air Asia, the other associate companies had not performed well. However, with the current low oil price, the odds of them turning around had improved substantially. In coming quarters, we will find out whether that will indeed be the case.

(d) In FY2009, the group undertook a placement exercise involving issuance of 380 mil new shares at RM1.33 per share to raise RM500 mil. Apart from that, there is no other equity fund raising exercise. Seemed like "rights issue every now and then" is nothing more than wild talks.

(e) Not only that, Air Asia has been consistently paying out dividend since FY2011.

With prevailing low oil price and expected spike in earnings, shareholders will be looking forward to generous payout going forward. Why not ? Tony loves cash too.

Cheers.

No comments:

Post a Comment