Author: Icon8888 | Publish date: Thu, 23 Jun 2016, 06:44 AM

First of all, I would like to clarify that the title of my article is not meant to scold or insult anybody. It was borrowed from Bill Clinton's presidential campaign in the 90s.

"IT IS THE ECONOMY THAT MATTERS, STUPID"

Clinton was campaigning against President George W. Bush (Senior). The word "Stupid" was used to drive home the message that of all the issues that are relevant, it is the economy that determines whether the country is heading in the right direction. As we all know, Clinton won the election.

Ok, now let's get back to the main business.

In this article, I will discuss the stock picking strategy of several forum members in i3 - Icon8888, Stockmanmy, Uncle Koon, KC Chong, Calvin Tan.

On surface, these few people have different ways of picking stocks. But I would like to argue that if you strip away all the intricacies, they all reveal a similar set of beating hearts.

To find out more, please read on.

1. Icon8888 - Laser Beam Focus On Future Earnings

Icon pick stocks based on the expectation he has for the PLC's future earnings. I think this has been made very clear through his various articles, no need to further elaborate.

2. Stockmanmy - Brutally Honest

Stockmanmy joined i3 not too long ago. He started by advocating that successful stockpicking is related to concepts like "sound portfolio management", "successful investors must have conviction", etc, etc.

But I believe those are no more his core ideologies. Last week, in his article "so you want to become value investors ? (6)", he loudly declared that "the best predictor of share price is earning growth".

THAT, put him in the same camp as Icon.

(But Icon doesn't endorse the harsh way he treated KC Chong in his article)

3. Uncle Koon - Ate Dead Cats

In Chinese, "eat dead cats" means being held responsible for mistakes / crime not committed by you.

When come to Uncle Koon, I must tread carefully. Many forum members are VERY angry with him. The crowd is not always rationale. There is currently a sentiment of "If you are not with us, you are against us" in the forum. Whoever that dares to side with him or stay neutral will be deemed as public enemy.

Well, I don't want to play any part in this messy affair. However, I would like to broadly dissect the issues into two major components :-

(a) Uncle Koon misbehaved YES, I agree with this. A lot of the things that Uncle Koon had done in the past is not beyond reproach, especially his non diclosure of changes in major shareholding. Naughty !!! Evil !!! Bad !!!

(b) Uncle Koon caused us to lose money NO, he didn't.

Actually, item (b) above is the reason I rope in Uncle Koon for discussion in this article. The message is this :

"What caused you to lose money is not because of the various little things that Uncle Koon had done. Those little things are irritating. But they played very minor role in your misfortune.

What caused you to lose money is the PLC that you invest in DIDN'T DELIVER STRONG PROFIT AS EXPECTED".

Let's take Can One as an example.

Quarter Result:

If you compared the earnings table and the chart above, Canone share price experienced strong run around November 2015, after releasing two consecutive quarters of strong results - June 2015 quarter's strong profit caused certain people to start accumulating. September 2015 quarter's strong profit "confirm a trend", resulting in massive buying by the investing public.

However, after a good run, Canone share price started declining in February 2016. That was actually due to the release of December 2015 quarterly result, which was below everybody's expectation. Share price declined further in May 2016 after the release of another quarter (March 2016) of depressing results.

See the correlation ? Strong earnings caused share price to go up, weak earnings caused share price to go down.

What was Uncle Koon's role in this ? Very minimal. We don't know whether his selling (secret selling ?), if any, caused Canone share price to decline. But without Uncle Koon, the same would have happened. Some other investors would have filled his role and pressed the Sell button.

There are two sides to every coin. The same is true for price going up. Uncle Koon went around town to claim credit for "helping many people to make money". I would like to contend that the majority of the credit should go to the PLC. It is their sterling performance that make those people rich, not Uncle Koon. Uncle Koon is a tour guide that brings you to a good restaurant. It is the skill of the cook that impress you, not the tour guide.

Summary conclusion - It is not my intention to defend Uncle Koon for his "misbehavior". It is also not my intention to deny him the credit that he deserves. The main purpose of me writing this section is to highlight the major role corporate earnings play in determining share price.

Bear this in mind the next time you want to buy a stock - "It is the future earning that matters, stupid"

4. KC Chong - The Republican That Secretly Votes For Democrats

When come to KC, what is your impression of his style of investment ? How about the following stereotype ?

(i) He analysed PLCs by using HISTORICAL financial ratios such as Earnings Yield, EV / EBITDA, ROIC, etc. Based on those ratios, he makes decisions to buy, hold and sell.

(ii) Very averse to making prediction about the future. His famous quote is "there is no statistical significance that anyone can predict the future".

In a nutshell, "KC relies heavily on past performance of PLCs to guide his investment decisions".

Is that really the case ? If I ask 100 people here in i3, probably 99 will say Yes. If I ask the same question to KC, he probably will say Yes too !

I used to have that perception too. However, yesterday I went through 221 articles posted by KC in his blog, printed some out and read them carefully. After doing that, I have a different understanding of KC (which KC himself probably isn't aware of).

My hypothesis : "Contrary to his own belief that one should not invest based on prediction of future, KC subsconsciuosly does so".

In other words, "prediction of future" does play a significant role in KC's stockpicking.

What made me came up with such hypothesis ? Just look at his recent stock pick, which he displayed in one of his recent article :-

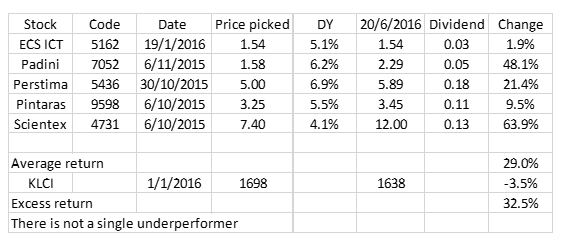

The interesting thing about the table above is not what is in there. The interesting thing is what is NOT there.

The portfolio above, which has performed very well (29% return), contains two retailers (ECS ICT and Padini), two manufacturers (Perstima and Scientex) and a contractor (Pintaras).

IT DOES NOT CONTAIN ANY PROPERTY DEVELOPER, PLANTATION COMPANY, OIL AND GAS COMPANY OR AUTO COMPANY, ALL OF WHICH ARE CURRENTLY FACING CHALLENGING OPERATING ENVIRONMENT.

If KC's style is indeed PAST driven, he would have included some of those companies in his portoflio. Many stocks in those industries are trading at depressed level and should be flashing Buy signals from historical ROIC, EV multiples or Earnings Yield point of view.

(Before I proceed further, let me get one thing straight - KC CHONG WILL NOT LIE TO US. The last thing in this world that I will do is to suspect that KC is being hypocritical by preaching about the importance of the past while secretly investing based on the future. What benefit does he get by twist and turn like that ?)

In my opinion, KC sincerely believes in what he taught, that one should place relatively high weightage on the past. Of course, there is no way I can know how he ended up with this style. Maybe due to his passion of learning from Gurus ? Maybe it gives him more comfort ? Maybe his previous success reinforced his belief ?

Whatever it is, and irregardless of whether KC agrees with me or not, my observation is thatmost of us, when come to picking stocks, will steal a glance at the future, even if we openly declare that we are not interested in it.

We Might Be More Similar Than We Think

Now let's go back to discuss the recent skirmishes between Stockmanmy and KC Chong. Stockmanmy complained that KC relied too much on a bunch of historical financial ratios. According to him, it is better to invest based on future earnings. KC stood his ground and countered that "there is no statistical significance that one can predict the future".

So, who is right ? Whose method is better ?

In my opinion, it is a false choice - neither is more superior than the other. THE TWO METHODS ARE MORE SIMILAR TO EACH OTHER THAN THEY THINK.

Let's take Scientex as an example. Both Stockmanmy and KC like this stock.

Stockmanmy is very straightforward, he believes future earnings is key. Scientex delivered strong earnings recently. Stockmanmy thinks it is likely to continue in the future. So it is his type of stock - BUY.

KC is different. He will pull out his spreadsheet and start crunching numbers. Finally the numbers came out, he looked at it, nod with satisfaction and called his remisier to place a Buy order.

On the surface, the two are different - Stockmanmy placed a Buy order without paying attention to ROIC, EV/BITDA, EY, etc while KC ran all those numbers, satisfied with them, only then he placed a Buy order.

However, if you think about it, that difference is actually superficial.

KC Chong is not a computer. He did not scan through all 3,000 counters in Bursa (compute their ROIC, EY, etc) to single out Scientex. What motivated him to take a close look at Scientex in the first place ? It is actually the AWARENESS of the bright prospects of Scientex that prompted him to study it. He most likely get the leads from bits and pieces of information that he gathered from various sources :-

(i) Scientex recently announced a strong set of results;

(ii) Details about Scientex's capital expenditure program; and

(iii) Details about how the recent weakening of Ringgit has made Scientex's export business very profitable.

In other words, before he ran the financial ratios such as ROIC, EY, etc, KC has more or less already known that Scientex will have strong future earnings. Those ratios merely confirm what he suspected and gave him additional comfort.

In other words, KC is more "future oriented" than he is aware of. That makes him more or less the same as Stockmanmy.

That is why I said the two gentlemen shared more similarities than they are aware of.

5. Calvin Tan - NTA Based Investing

Calvin's style of investment is the exact opposite of what I describe in this article. He invests mostly based on NTA.

Calvin claims that he has high success rate, but many people might not agree with him on that.

One successful case often quoted by Calvin is Super Enterprise, which he has been calling for buy at around RM1.00. Super Enterprise subsequently went up to RM3.80 when an American company offered to take it over by cash.

Is this the long awaited proof that picking stocks based on NTA works ? I am curious, so I undertook a study of Super Enterprise's case. To my surprise, my study leads to an exact opposite conclusion - buying stocks based on NTA does not work, it is earnings that matters.

To understand how I arrive at such a conclusion, please refer to table and chart below.

Quarter Result:

As shown in the chart above, from 2011 until early 2015, Super Enterprise's share price stagnated at around RM1.00.

In April 2015, Super Enterprise received an offer from an Amercian company to take it over at RM3.80 per share. Share price spiked to reflect the unlocking of value.

The offer from the American buyer did not come out of no where for no reason.

By Q4 of 2014, oil price started declining sharply. As Super Enterprise uses petroleum byproducts as raw material, its profit margin improved substantially. In the December 2014 quarter, Super Enterprise reported an all time high EPS of 7.57 sen.

My guess is that the American buyer saw the bright prospect of the industry ahead and decided to act decisively to take over Super Enterprise (probably as a way to quickly expand production capacity).

I made the following key observations from the above case :-

(i) Despite trading at deep discount to NTA, investors are not interested in Super Enterprise. During the 4 year period from 2011 until 2015, stock price stagnated at around RM1.00.

(ii) The moment Super Enterprise's earning prospect showed sign of improvement, the stock immediately attracted attention from the American buyer, which is a competitor operating in the same industry.

Based on the foregoing, can you blame me if I say that when we pick stocks, the most important thing to look out for is future earning, and not NTA ?

What About Benjamin Graham ?

I can refuse to believe that NTA based investing has high success rate, but this is the same method that Benjamin Graham has been preaching. Is Icon8888 saying that Benjamin Graham was wrong, and Icon8888 is right ?

Not really. Graham was not wrong. His method worked well during his time (the 1930s). However, as the field of Finance evolves over the years, Graham's method might have become a littlle bit obsolete. I did not simply jump into that conclusion. Joel Greenblatt was the one that said that (in his book) :-

Expectation of Modern Day Investors

During Graham's time (1930s), finance theory was still in its infancy. A company's value is in its tangible assets. However, over the subsequent decades, finance theory has evolved substantially. With the advent of the concept of Time Value of Money (and its spin offs, Discounted Cash Flow and Net Present Value), it was increasingly recognized that profit and cash flow stream is more reflective of a company's intrinsic value than tangible assets.

Concepts like these are well understood even in developing countries like Malaysia. Nowadays, investors are increasingly paying more attention to dividend. To pay out dividend, the company must be generating profit.

With common understanding like that, no wonder modern day investors crave profit and are indifferent towards NTA.

6. Concluding Remarks

(a) In this article, I try to convince readers that the best way to pick stocks is to focus on a company's future earnings.

(b) However, the million dollar question is "can ordinary investors like us predict future earning ?". Based on my experience so far in the market, most of the time we cannot predict the future. However, occasionally, a window will open and allow us to see things with relatively good clarity. When a window opens in front of you, you should act on the opportunities.

One good example is Air Asia. The group's operating environment has improved substantially recently. This was followed by its controlling shareholders willing to commit huge capital to increase their shareholding. Putting all these together, there is reasonable odds that the company will do well going forward. It is rational to seize the moment and overweight the stock.

(c) As for NTA based investing. My experience so far has not been positive. As far as I am concerned, I prefer to stick to earning related methods.

However, there is still one anomaly that prevents me from declaring that NTA method is dead - Walter Schloss. Walter Scholss is a very successful investor and he did it by investing in stocks trading at deep discount to NTA. I tried to study his portfolio but unfortunately cannot find a book that can provide the details. I will write about him if I can find out more details in the future.

Have a nice day.

"IT IS THE ECONOMY THAT MATTERS, STUPID"

Clinton was campaigning against President George W. Bush (Senior). The word "Stupid" was used to drive home the message that of all the issues that are relevant, it is the economy that determines whether the country is heading in the right direction. As we all know, Clinton won the election.

Ok, now let's get back to the main business.

In this article, I will discuss the stock picking strategy of several forum members in i3 - Icon8888, Stockmanmy, Uncle Koon, KC Chong, Calvin Tan.

On surface, these few people have different ways of picking stocks. But I would like to argue that if you strip away all the intricacies, they all reveal a similar set of beating hearts.

To find out more, please read on.

1. Icon8888 - Laser Beam Focus On Future Earnings

Icon pick stocks based on the expectation he has for the PLC's future earnings. I think this has been made very clear through his various articles, no need to further elaborate.

2. Stockmanmy - Brutally Honest

Stockmanmy joined i3 not too long ago. He started by advocating that successful stockpicking is related to concepts like "sound portfolio management", "successful investors must have conviction", etc, etc.

But I believe those are no more his core ideologies. Last week, in his article "so you want to become value investors ? (6)", he loudly declared that "the best predictor of share price is earning growth".

THAT, put him in the same camp as Icon.

(But Icon doesn't endorse the harsh way he treated KC Chong in his article)

3. Uncle Koon - Ate Dead Cats

In Chinese, "eat dead cats" means being held responsible for mistakes / crime not committed by you.

When come to Uncle Koon, I must tread carefully. Many forum members are VERY angry with him. The crowd is not always rationale. There is currently a sentiment of "If you are not with us, you are against us" in the forum. Whoever that dares to side with him or stay neutral will be deemed as public enemy.

Well, I don't want to play any part in this messy affair. However, I would like to broadly dissect the issues into two major components :-

(a) Uncle Koon misbehaved YES, I agree with this. A lot of the things that Uncle Koon had done in the past is not beyond reproach, especially his non diclosure of changes in major shareholding. Naughty !!! Evil !!! Bad !!!

(b) Uncle Koon caused us to lose money NO, he didn't.

Actually, item (b) above is the reason I rope in Uncle Koon for discussion in this article. The message is this :

"What caused you to lose money is not because of the various little things that Uncle Koon had done. Those little things are irritating. But they played very minor role in your misfortune.

What caused you to lose money is the PLC that you invest in DIDN'T DELIVER STRONG PROFIT AS EXPECTED".

Let's take Can One as an example.

Quarter Result:

| Quarter | Revenue ('000) | Profit Attb. to SH ('000) | EPS (Cent) |

|---|---|---|---|

| 2016-03-31 | 204,891 | 10,953 | 5.70 |

| 2015-12-31 | 236,260 | 13,938 | 7.25 |

| 2015-09-30 | 242,353 | 27,446 | 14.28 |

| 2015-06-30 | 216,568 | 23,670 | 14.77 |

| 2015-03-31 | 191,292 | 15,053 | 9.88 |

If you compared the earnings table and the chart above, Canone share price experienced strong run around November 2015, after releasing two consecutive quarters of strong results - June 2015 quarter's strong profit caused certain people to start accumulating. September 2015 quarter's strong profit "confirm a trend", resulting in massive buying by the investing public.

However, after a good run, Canone share price started declining in February 2016. That was actually due to the release of December 2015 quarterly result, which was below everybody's expectation. Share price declined further in May 2016 after the release of another quarter (March 2016) of depressing results.

See the correlation ? Strong earnings caused share price to go up, weak earnings caused share price to go down.

What was Uncle Koon's role in this ? Very minimal. We don't know whether his selling (secret selling ?), if any, caused Canone share price to decline. But without Uncle Koon, the same would have happened. Some other investors would have filled his role and pressed the Sell button.

There are two sides to every coin. The same is true for price going up. Uncle Koon went around town to claim credit for "helping many people to make money". I would like to contend that the majority of the credit should go to the PLC. It is their sterling performance that make those people rich, not Uncle Koon. Uncle Koon is a tour guide that brings you to a good restaurant. It is the skill of the cook that impress you, not the tour guide.

Summary conclusion - It is not my intention to defend Uncle Koon for his "misbehavior". It is also not my intention to deny him the credit that he deserves. The main purpose of me writing this section is to highlight the major role corporate earnings play in determining share price.

Bear this in mind the next time you want to buy a stock - "It is the future earning that matters, stupid"

4. KC Chong - The Republican That Secretly Votes For Democrats

When come to KC, what is your impression of his style of investment ? How about the following stereotype ?

(i) He analysed PLCs by using HISTORICAL financial ratios such as Earnings Yield, EV / EBITDA, ROIC, etc. Based on those ratios, he makes decisions to buy, hold and sell.

(ii) Very averse to making prediction about the future. His famous quote is "there is no statistical significance that anyone can predict the future".

In a nutshell, "KC relies heavily on past performance of PLCs to guide his investment decisions".

Is that really the case ? If I ask 100 people here in i3, probably 99 will say Yes. If I ask the same question to KC, he probably will say Yes too !

I used to have that perception too. However, yesterday I went through 221 articles posted by KC in his blog, printed some out and read them carefully. After doing that, I have a different understanding of KC (which KC himself probably isn't aware of).

My hypothesis : "Contrary to his own belief that one should not invest based on prediction of future, KC subsconsciuosly does so".

In other words, "prediction of future" does play a significant role in KC's stockpicking.

What made me came up with such hypothesis ? Just look at his recent stock pick, which he displayed in one of his recent article :-

The interesting thing about the table above is not what is in there. The interesting thing is what is NOT there.

The portfolio above, which has performed very well (29% return), contains two retailers (ECS ICT and Padini), two manufacturers (Perstima and Scientex) and a contractor (Pintaras).

IT DOES NOT CONTAIN ANY PROPERTY DEVELOPER, PLANTATION COMPANY, OIL AND GAS COMPANY OR AUTO COMPANY, ALL OF WHICH ARE CURRENTLY FACING CHALLENGING OPERATING ENVIRONMENT.

If KC's style is indeed PAST driven, he would have included some of those companies in his portoflio. Many stocks in those industries are trading at depressed level and should be flashing Buy signals from historical ROIC, EV multiples or Earnings Yield point of view.

(Before I proceed further, let me get one thing straight - KC CHONG WILL NOT LIE TO US. The last thing in this world that I will do is to suspect that KC is being hypocritical by preaching about the importance of the past while secretly investing based on the future. What benefit does he get by twist and turn like that ?)

In my opinion, KC sincerely believes in what he taught, that one should place relatively high weightage on the past. Of course, there is no way I can know how he ended up with this style. Maybe due to his passion of learning from Gurus ? Maybe it gives him more comfort ? Maybe his previous success reinforced his belief ?

Whatever it is, and irregardless of whether KC agrees with me or not, my observation is thatmost of us, when come to picking stocks, will steal a glance at the future, even if we openly declare that we are not interested in it.

We Might Be More Similar Than We Think

Now let's go back to discuss the recent skirmishes between Stockmanmy and KC Chong. Stockmanmy complained that KC relied too much on a bunch of historical financial ratios. According to him, it is better to invest based on future earnings. KC stood his ground and countered that "there is no statistical significance that one can predict the future".

So, who is right ? Whose method is better ?

In my opinion, it is a false choice - neither is more superior than the other. THE TWO METHODS ARE MORE SIMILAR TO EACH OTHER THAN THEY THINK.

Let's take Scientex as an example. Both Stockmanmy and KC like this stock.

Stockmanmy is very straightforward, he believes future earnings is key. Scientex delivered strong earnings recently. Stockmanmy thinks it is likely to continue in the future. So it is his type of stock - BUY.

KC is different. He will pull out his spreadsheet and start crunching numbers. Finally the numbers came out, he looked at it, nod with satisfaction and called his remisier to place a Buy order.

On the surface, the two are different - Stockmanmy placed a Buy order without paying attention to ROIC, EV/BITDA, EY, etc while KC ran all those numbers, satisfied with them, only then he placed a Buy order.

However, if you think about it, that difference is actually superficial.

KC Chong is not a computer. He did not scan through all 3,000 counters in Bursa (compute their ROIC, EY, etc) to single out Scientex. What motivated him to take a close look at Scientex in the first place ? It is actually the AWARENESS of the bright prospects of Scientex that prompted him to study it. He most likely get the leads from bits and pieces of information that he gathered from various sources :-

(i) Scientex recently announced a strong set of results;

(ii) Details about Scientex's capital expenditure program; and

(iii) Details about how the recent weakening of Ringgit has made Scientex's export business very profitable.

In other words, before he ran the financial ratios such as ROIC, EY, etc, KC has more or less already known that Scientex will have strong future earnings. Those ratios merely confirm what he suspected and gave him additional comfort.

In other words, KC is more "future oriented" than he is aware of. That makes him more or less the same as Stockmanmy.

That is why I said the two gentlemen shared more similarities than they are aware of.

5. Calvin Tan - NTA Based Investing

Calvin's style of investment is the exact opposite of what I describe in this article. He invests mostly based on NTA.

Calvin claims that he has high success rate, but many people might not agree with him on that.

One successful case often quoted by Calvin is Super Enterprise, which he has been calling for buy at around RM1.00. Super Enterprise subsequently went up to RM3.80 when an American company offered to take it over by cash.

Is this the long awaited proof that picking stocks based on NTA works ? I am curious, so I undertook a study of Super Enterprise's case. To my surprise, my study leads to an exact opposite conclusion - buying stocks based on NTA does not work, it is earnings that matters.

To understand how I arrive at such a conclusion, please refer to table and chart below.

Quarter Result:

| Quarter | Revenue ('000) | Profit Attb. to SH ('000) | EPS (Cent) | DPS (Cent) | NAPS | |

|---|---|---|---|---|---|---|

| 2015-06-30 | 36,146 | 2,293 | 5.50 | - | 2.4700 | |

| 2015-03-31 | 35,910 | 2,973 | 7.12 | - | 2.4100 | |

| 2014-12-31 | 35,523 | 3,160 | 7.57 | - | 2.3200 | |

| 2014-09-30 | 35,898 | 2,001 | 4.79 | - | 2.2800 | |

| 2014-06-30 | 32,656 | 1,384 | 3.31 | - | 2.2300 | |

| 2014-03-31 | 30,364 | 3,050 | 7.29 | - | - | |

| 2013-12-31 | 30,554 | 924 | 2.21 | - | 2.1300 | |

| 2013-09-30 | 31,827 | 1,327 | 3.17 | - | 2.1500 | |

| 2013-06-30 | 31,139 | 2,028 | 4.85 | - | 2.1300 |

As shown in the chart above, from 2011 until early 2015, Super Enterprise's share price stagnated at around RM1.00.

In April 2015, Super Enterprise received an offer from an Amercian company to take it over at RM3.80 per share. Share price spiked to reflect the unlocking of value.

The offer from the American buyer did not come out of no where for no reason.

By Q4 of 2014, oil price started declining sharply. As Super Enterprise uses petroleum byproducts as raw material, its profit margin improved substantially. In the December 2014 quarter, Super Enterprise reported an all time high EPS of 7.57 sen.

My guess is that the American buyer saw the bright prospect of the industry ahead and decided to act decisively to take over Super Enterprise (probably as a way to quickly expand production capacity).

I made the following key observations from the above case :-

(i) Despite trading at deep discount to NTA, investors are not interested in Super Enterprise. During the 4 year period from 2011 until 2015, stock price stagnated at around RM1.00.

(ii) The moment Super Enterprise's earning prospect showed sign of improvement, the stock immediately attracted attention from the American buyer, which is a competitor operating in the same industry.

Based on the foregoing, can you blame me if I say that when we pick stocks, the most important thing to look out for is future earning, and not NTA ?

What About Benjamin Graham ?

I can refuse to believe that NTA based investing has high success rate, but this is the same method that Benjamin Graham has been preaching. Is Icon8888 saying that Benjamin Graham was wrong, and Icon8888 is right ?

Not really. Graham was not wrong. His method worked well during his time (the 1930s). However, as the field of Finance evolves over the years, Graham's method might have become a littlle bit obsolete. I did not simply jump into that conclusion. Joel Greenblatt was the one that said that (in his book) :-

Expectation of Modern Day Investors

During Graham's time (1930s), finance theory was still in its infancy. A company's value is in its tangible assets. However, over the subsequent decades, finance theory has evolved substantially. With the advent of the concept of Time Value of Money (and its spin offs, Discounted Cash Flow and Net Present Value), it was increasingly recognized that profit and cash flow stream is more reflective of a company's intrinsic value than tangible assets.

Concepts like these are well understood even in developing countries like Malaysia. Nowadays, investors are increasingly paying more attention to dividend. To pay out dividend, the company must be generating profit.

With common understanding like that, no wonder modern day investors crave profit and are indifferent towards NTA.

6. Concluding Remarks

(a) In this article, I try to convince readers that the best way to pick stocks is to focus on a company's future earnings.

(b) However, the million dollar question is "can ordinary investors like us predict future earning ?". Based on my experience so far in the market, most of the time we cannot predict the future. However, occasionally, a window will open and allow us to see things with relatively good clarity. When a window opens in front of you, you should act on the opportunities.

One good example is Air Asia. The group's operating environment has improved substantially recently. This was followed by its controlling shareholders willing to commit huge capital to increase their shareholding. Putting all these together, there is reasonable odds that the company will do well going forward. It is rational to seize the moment and overweight the stock.

(c) As for NTA based investing. My experience so far has not been positive. As far as I am concerned, I prefer to stick to earning related methods.

However, there is still one anomaly that prevents me from declaring that NTA method is dead - Walter Schloss. Walter Scholss is a very successful investor and he did it by investing in stocks trading at deep discount to NTA. I tried to study his portfolio but unfortunately cannot find a book that can provide the details. I will write about him if I can find out more details in the future.

Have a nice day.

Great info! Very simple and easy…nobody can explain as interesting as this. I appreciate your time and effort on making things simple and easily understandable.

ReplyDeleteMoney Exchange In San Francisco